How AI Changes the Way Traders See Markets

What does AI actually change in trading?

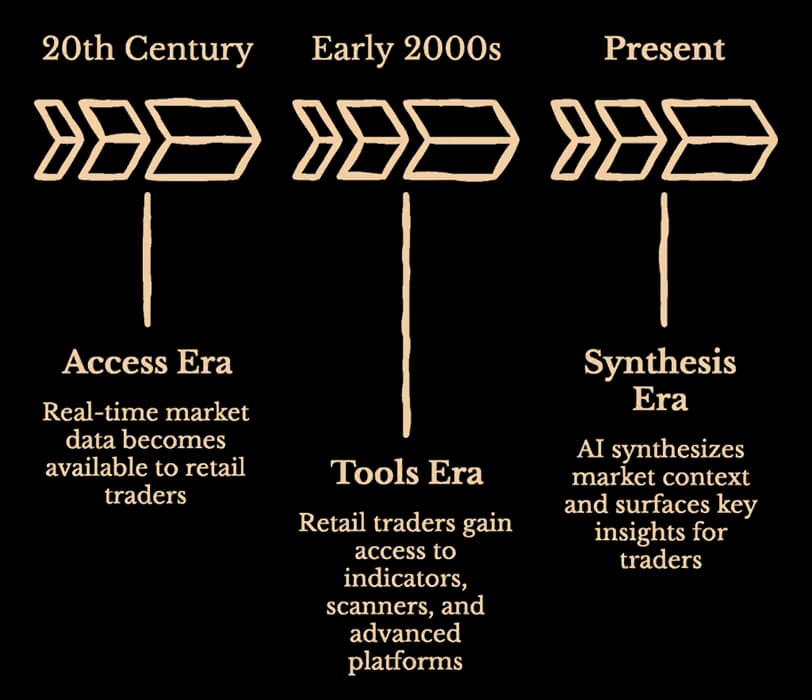

Three eras shape the answer. The first solved access — live data went from institutional privilege to default by the early 2000s. The second piled on tools, with every panel built on the assumption that the trader does the synthesis. The third is synthesis itself. AI isn't prediction — it's holding more context simultaneously than human working memory allows, then surfacing the parts that matter right now. The trader still decides. What changes is whether the picture they decide from is complete. Six-tab pre-market scanning collapses into one question that integrates price, flow, options positioning, and structure.

It's 8:47 AM. Markets open in thirteen minutes, and you're trying to build a directional bias on NIFTY from sources that don't talk to each other. TradingView says one thing, the options chain says another, the Telegram group is split three ways, and the 15-minute chart still doesn't agree with the 5-minute. Thirteen minutes is never enough to reconcile all of it, and the reason isn't discipline or screen time or strategy. It's that the workflow was designed to display information, not synthesise it, and every year traders add more panels without fixing the underlying problem. AI is the first development in twenty years that addresses that problem at the root, which is why understanding what it actually changes, specifically and mechanically, matters more right now than any particular setup or indicator.

Three Eras, Each Solving the Wrong Problem

The first era was access. Through most of the 20th century, real-time market data was an institutional privilege. Retail traders worked from delayed quotes and end-of-day prices. The information gap between a professional desk and an individual trader was enormous, and it came down almost entirely to one thing: who could see prices as they happened. The internet closed that gap faster than anyone expected. By the early 2000s, live quotes, basic charting, and electronic execution were available to anyone with a brokerage account. An asymmetry that had taken decades to build dissolved in a few years.

The second era was tools. Once data access equalised, competition shifted to analytical capability. Platforms added indicators, screeners, options analytics, and scanners. The trader who could use more tools more effectively had an edge, and the industry responded with an arms race of dashboards, each adding panels, views, and data sources. This is still broadly the era most traders are operating in, and it produced real improvements. Retail traders today have access to analytical tools that would have looked institutional a decade ago.

But the tools era created a problem it couldn't solve from within. Every new panel, every new data source added to a trading platform, assumed the same thing: that the human trader would do the synthesis. The workflow kept expanding. The synthesis engine, which is a trader's brain under time pressure with money at risk, didn't.

The third era is synthesis. Not more data displayed, but data integrated. That distinction is what this piece is about.

The Dashboard Was Always a Workaround

The assumption behind every trading dashboard ever built is that the human is the synthesis engine, and that assumption held up until traders had too many things to monitor simultaneously, and then it quietly broke.

When traders had two or three sources to track, the assumption was fine. It breaks down at seven. A serious NIFTY options trader during a live session is simultaneously tracking price action across three timeframes, open interest at key strikes, put/call ratio, India VIX, order flow, sector rotation between Banking and IT, and any breaking macro news. None of these panels communicate with each other. The trader mentally stitches them together on every decision, under time pressure, with real money on the line. An SPY trader in the US is doing the same thing across their own stack of fragmented tools, arriving at the same structural problem through a different set of tickers.

The result isn't bad trading. Plenty of traders have built profitable processes within these constraints. But it is structurally incomplete trading, not because of effort or skill, but because the workflow was never designed to produce a synthesised picture. It was designed to show you pieces and let you connect them.

SEBI's data makes the consequence concrete. In its 2023 study of retail F&O participants, SEBI found that 89% lost money over the study period, with aggregate losses exceeding ₹1.8 lakh crore across three years. The standard reading is that retail traders lack discipline or strategy. The more accurate reading is that retail traders have been operating with structurally inferior analytical infrastructure, not inferior effort or intentions, while trading against participants who don't have that constraint. Adding more panels didn't fix the problem. It compounded it, because every new source was one more thing the trader had to manually integrate before clicking buy.

Synthesis Is Not Prediction, and the Difference Is Everything

What AI actually does in a trading context is hold more context simultaneously than any human can, then surface the parts of that context that matter right now. That's a precisely different claim from prediction, and the distinction changes what the tool is actually for.

A prediction tool claims to know the future, which should invite immediate scepticism from anyone who has traded long enough to see their own forecasts fail. A synthesis tool claims to show you what is currently happening across more dimensions than you can track alone, without making directional calls on your behalf. The second claim is more modest and considerably more useful, because it doesn't ask you to outsource your judgement. It asks you to apply your judgement to a more complete picture.

Think about how a doctor reads a patient's results. They don't predict whether the patient will recover. They synthesise the available evidence — the scan, the bloodwork, the history, the symptoms — into a coherent picture of what's happening right now, and that picture informs the treatment decision. The doctor still decides. AI in trading works the same way. Draconic, an AI trading intelligence platform, synthesises across 176 proprietary metrics in real time covering price dynamics, institutional flow, order flow, options positioning, and multi-timeframe structure, and integrates them into a single analytical view. The synthesis informs the decision. The trader decides.

What this changes at 8:47 AM is concrete. Instead of cycling through six sources trying to build a pre-market picture, a trader asks one question. "What's the context for NIFTY this morning?" The answer draws from every relevant dimension simultaneously, not as 176 separate readings but as an integrated view. The time saved is real. The more important change is completeness: a synthesis doesn't miss the OI concentration at a strike you didn't think to check, or the velocity anomaly in overnight futures that a manual scan wouldn't surface, because it isn't scanning the way a human scans. It's holding everything at once.

What You Stop Missing Pre-Market, Mid-Session, and After

The shift from scanning to synthesis changes each phase of the trading day, and the impact is less about speed than about what stops falling through the gaps.

Pre-market preparation feels the change most immediately. The goal is to build a directional bias and identify the levels that matter before the open. In a dashboard workflow that takes 20 to 30 minutes of cycling through sources, completeness still depends on what you thought to check. In a synthesis workflow, one question covers everything simultaneously. The time saving is a side effect. The real change is that you're no longer one forgotten tab away from missing something that mattered.

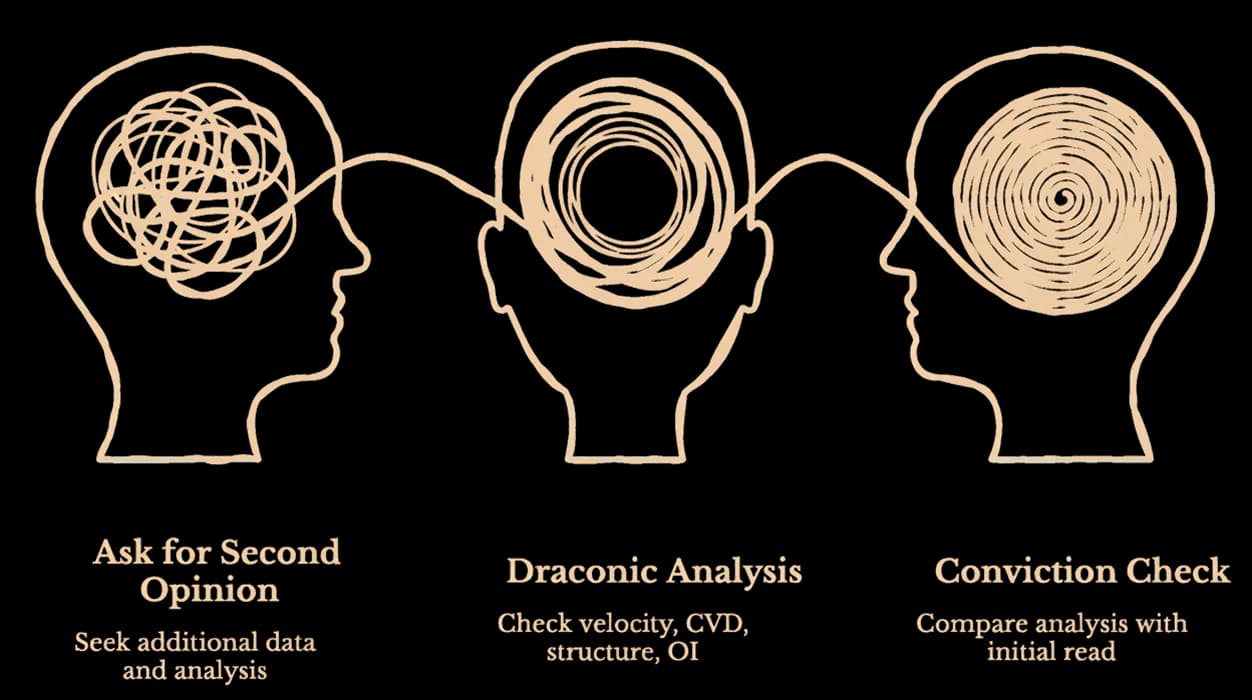

During the session, the shift is subtler but probably more consequential. Traders still watch their charts. The difference is what happens in the 30 seconds before a trade. Most traders at the moment of decision have a read on one or two dimensions, price structure, maybe a momentum indicator. They have a sense that something is setting up and they act on it with whatever context they've had time to build.

The second opinion workflow changes this. Before entering, a trader asks: "I'm looking at a demand zone on NIFTY at 22,400. What am I missing?" The synthesis checks velocity at the zone, CVD behaviour, higher timeframe structure, and OI positioning at nearby strikes. If everything agrees, conviction increases. If something conflicts, the trader knows before they click buy, not after. That's the use case: not replacing the trader's read, but completing it in the seconds before the decision actually matters.

Post-session, synthesis enables a review that fragmented tools genuinely can't. "What happened with NIFTY between 10:30 and 11:15 AM?" returns a coherent account drawn from a unified data view, not a reconstruction the trader builds from separate sources after the fact. Done consistently, that kind of structured review is where process improvements compound over time.

The Synthesis Gap Is What Institutions Don't Have Either

There's a version of this argument that goes: AI helps retail traders compete with institutions. That's partially true but misses the more interesting point — the synthesis gap isn't really an institutional vs. retail problem at all. It's a human cognitive architecture problem.

Institutional desks have speed advantages, capital advantages, and market access advantages that software doesn't equalise. Those gaps are structural. But the synthesis gap — the difference between what a system can hold in context and what a human can hold in context — is not an institutional vs. retail problem. Even a well-resourced professional trader is still a human trying to manually connect signals across multiple screens under time pressure.

What AI changes is not who has access to data. Retail traders have had data parity for over a decade. What AI changes is who can synthesise that data in real time, across more dimensions than human working memory allows, without missing the connection that changes the read.

That is a different conversation from "can retail beat institutions." It's the more tractable question of whether traders can make better-informed decisions than they currently do — and the answer, increasingly, is yes.

This Isn't Really a Retail vs. Institutions Story

The instinct is to frame AI as the great equaliser between retail traders and institutions, and that framing is partially right but misses the more interesting point.

Institutional desks have speed advantages, capital advantages, and market access advantages that software doesn't close. Those gaps are structural and they aren't closing. But the synthesis gap, the difference between what a system can hold in context and what a human can, isn't an institutional versus retail problem at all. It's a human cognitive architecture problem. Even a well-resourced professional trader is still a human trying to manually connect signals across multiple screens under time pressure. The ceiling on how much context a human can synthesise in real time doesn't change based on how much capital they're managing.

What changes isn't access to data. Retail traders have had data parity for over a decade. What changes is who can synthesise that data across more dimensions than working memory allows, without losing the connections that change the read. Good traders working with incomplete pictures make worse decisions than good traders working with complete ones, and closing that gap is more tractable than closing the institutional one by a significant margin.

The Analytical Ceiling Is Moving

Every major transition in trading history changed who could participate and how effectively. Floor trading gave way to electronic execution, which gave way to the dashboard era. Each transition reset the baseline for what serious trading required, and each one was irreversible once it happened.

This transition changes the analytical ceiling itself: how much context a trader holds at the moment a decision has to be made, how completely the available data gets synthesised before they act, how quickly they can move from raw information to a coherent read. The traders who adapt won't be the ones who add AI as another panel to an already-crowded dashboard. They'll be the ones who replace the scanning model with a synthesis-first workflow, and once you've worked that way for a month, going back feels like navigating with one eye closed.

More like this

May 12, 2026behind-the-price

Sector Rotation — The Macro Signal Most Traders Ignore

The Draconic Team • 3 min

May 11, 2026behind-the-price

How Market Makers Create Invisible Floors and Ceilings

The Draconic Team • 11 min

May 8, 2026behind-the-price

The Magnetic Levels — Why Price Gets Drawn to Certain Numbers Near Expiry

The Draconic Team • 8 min

May 7, 2026behind-the-price

When Three Flow Signals Agree Against Price

The Draconic Team • 4 min